Google vs. Yahoo

GOOG vs. YHOO – Main Event

Internet Giants Heavyweight Championship

“Are you ready to rumble?”

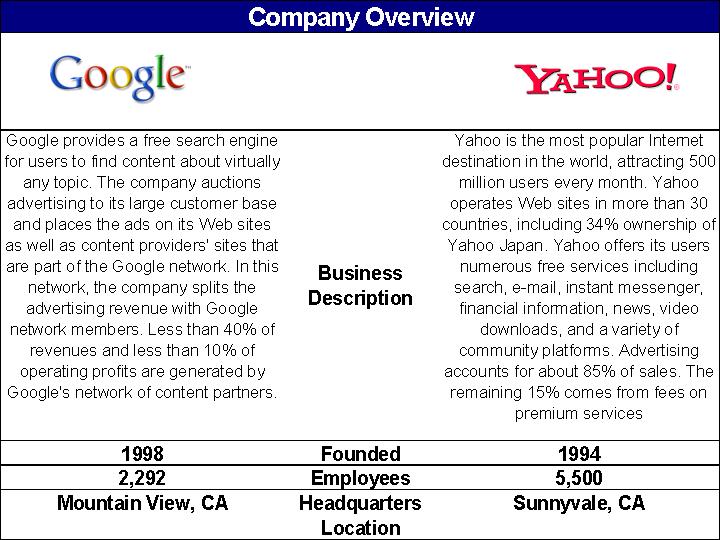

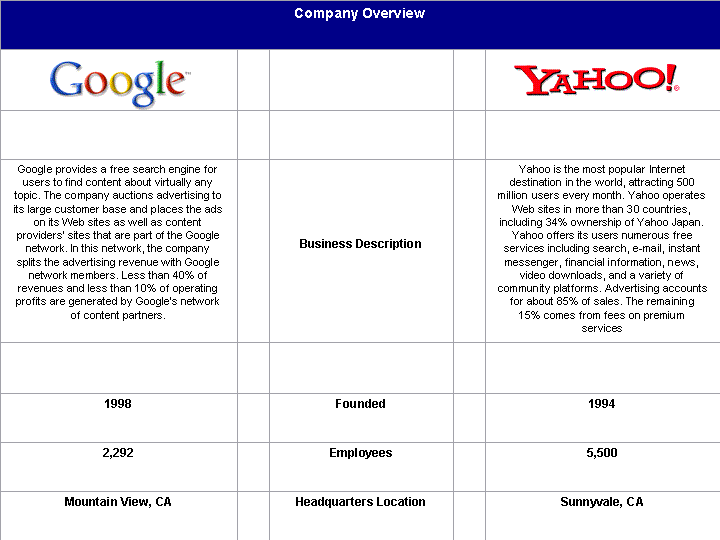

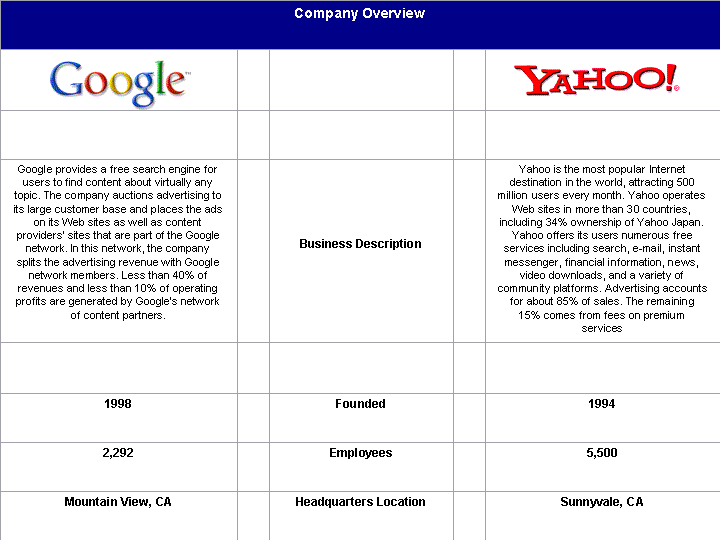

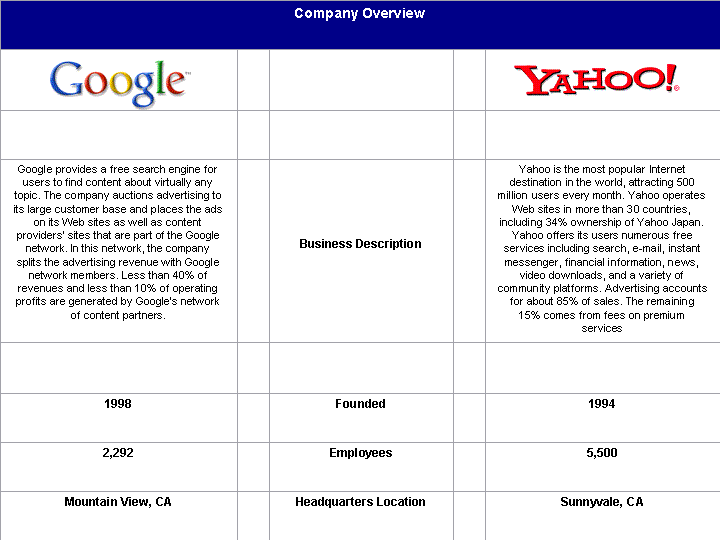

Let’s first look at the company overview to provide you with a background of the companies.

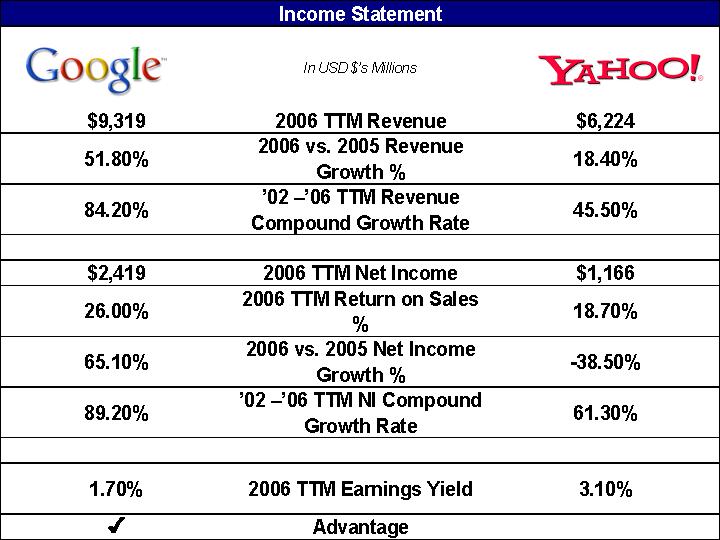

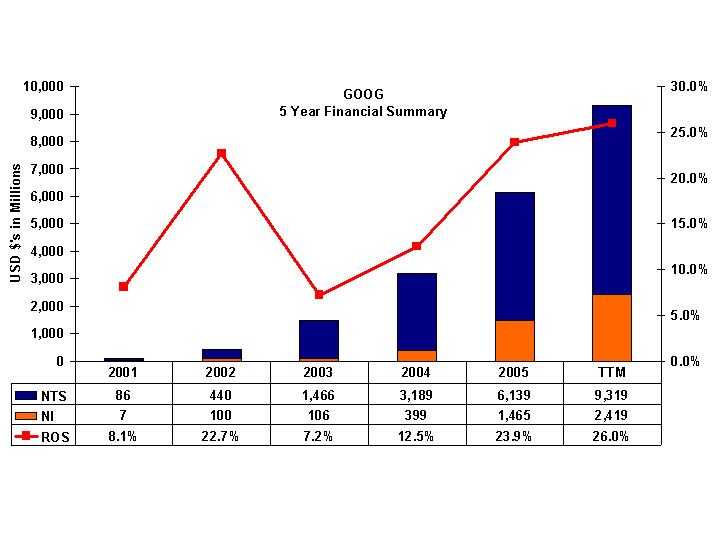

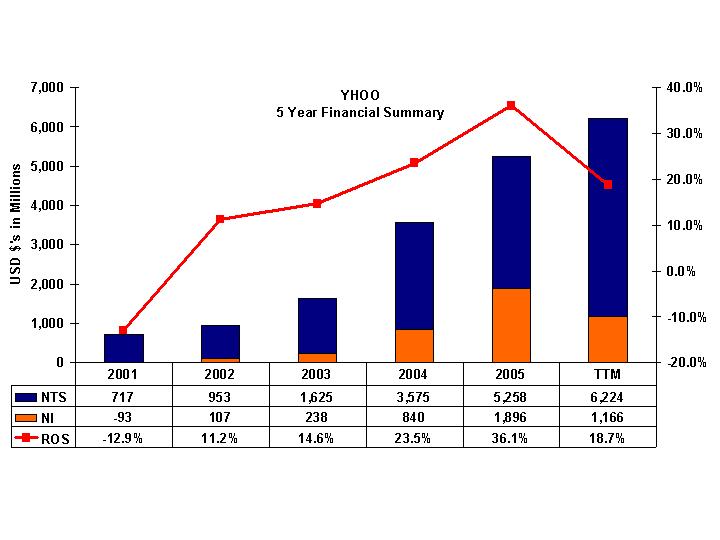

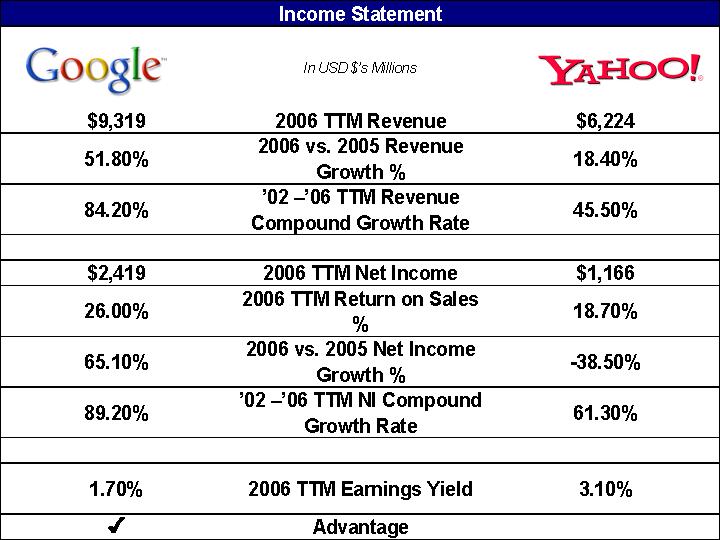

Round #1 - Income Statement, the clear winner is GOOG. With a commanding lead in all of the selected categories, the most impressive is the 5-year growth rate on revenue. In 2001, GOOG recorded $86MM of revenue compared to $717MM of revenue for YHOO. By the end of 2003, the two companies were almost equivalent in the amount of revenue recorded, with YHOO booking almost 2x of the net income. On a 2006 TTM basis, GOOG is recording approximately 33% more revenue than YHOO with an 800 basis point lead on margin, very impressive in the ability to drop most of the top line gains to the bottom line. To note, there are approximately one-time gains in YHOO’s 2005 financials that is reflecting the 2006 TTM annual growth rate to go negative.

Below you will find the Financial Trend Charts that I typically provide:

GOOG

YHOO

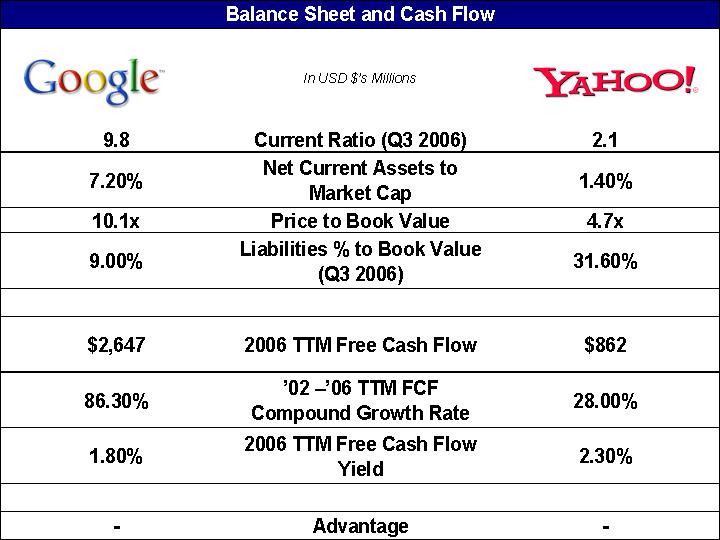

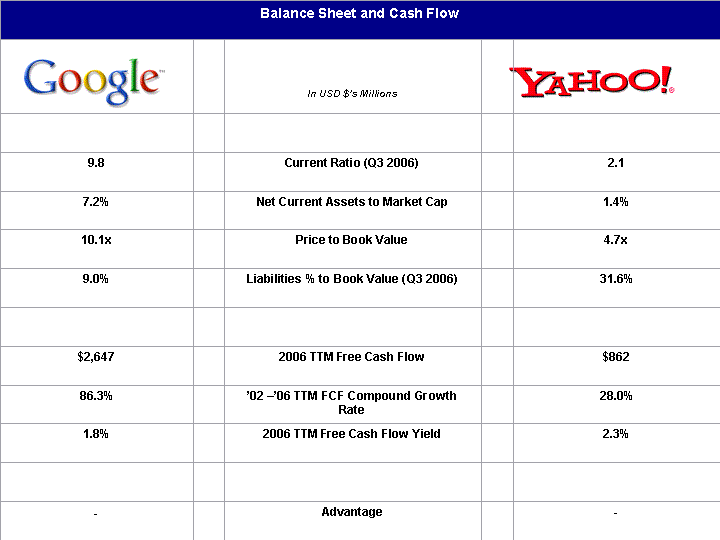

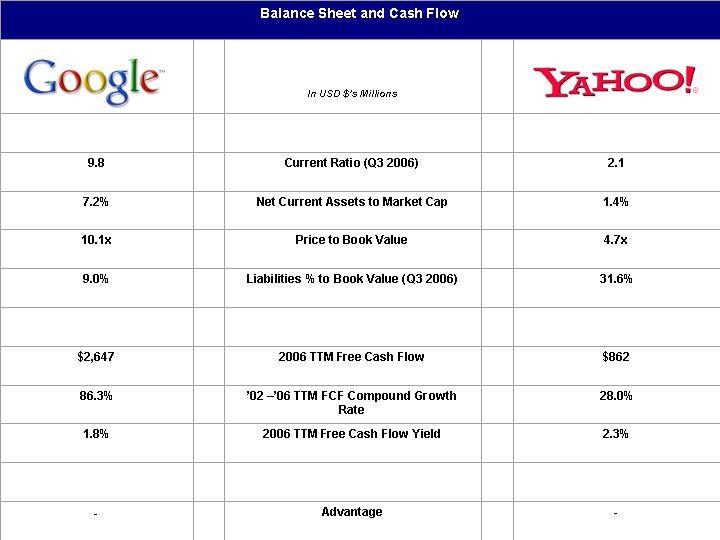

Round #2 - Balance Sheet & Cash Flow, I will rate a tie. GOOG is strong with the current ratio, net current assets, and the low amount of debt but YHOO is lower priced in the market with a better Price/Book and FCF yield. Either firm doesn’t pay a dividend. YHOO does carry some long-term debt on the books. Both firms can cover at least twice the level of the current liabilities, which doesn’t make them a concern for liquidity problems. In early October 2006, GOOG announced the acquisition of YouTube for $1.65 Billion in stock. I am surprised that GOOG decided to complete the acquisition with stock rather than use some of the $10.4 Billion in cash and marketable securities

What will GOOG do will all of that cash being generated???

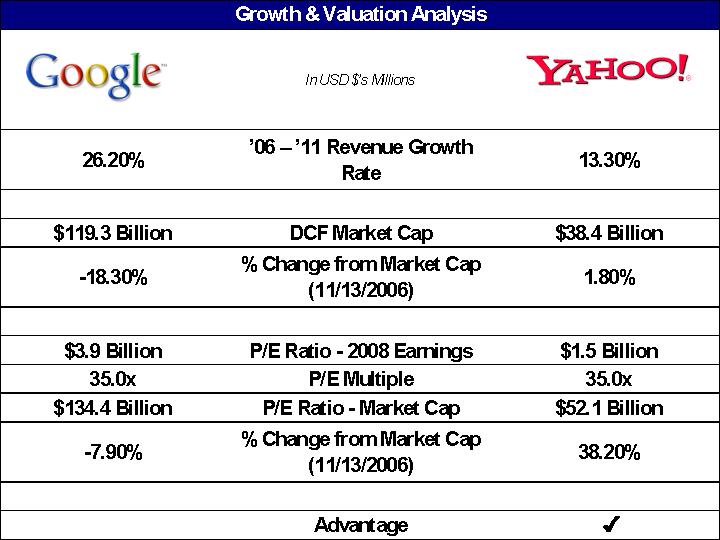

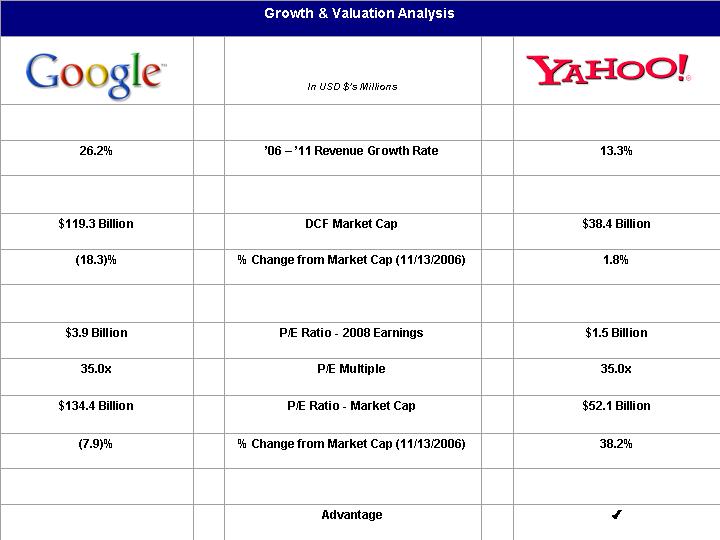

Round #3 – Growth & Valuation, YHOO currently holds some upside to the current trading levels. I am expecting GOOG to grow twice as fast as YHOO with both firms capturing approximately 30% of FCF to Revenue. Assuming a slightly higher WACC for Yahoo at 11.5% compared to GOOG’s 11.0% and both at 5% terminal value. With the above assumptions, GOOG is currently valuation is highlighting that these growth assumptions, and then some, are already priced into the market.

Sources:

Company websites

Edgar online database

Yahoo Finance

Morningstar

Barchart.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

2 comments:

Nice analysis.

Google is the better buy because they have a knack for dominating any marketplace they compete in.

Through strategic purchases like Youtube and the Firefox browser, Google is quickly building their search engine user base.

And not to mention how Adsense and Adwords have revolutionized the way internet users buy and place ads on webpages.

Yahoo! is trying to dip into Google's marketshare, but is their brand name big enough to lure Google users away from their easy to use and versatile platforms?

Don't think so.

I should have entered Google at $200 couple years ago, now I'm kicking myself.

Google is a good company.

Post a Comment